Fading Recovery?

As always, our Market Notes reports are available to you in PDF format. Click below to download.

Last year, we at Consilience Asset Management added a Macro-Economic component to our Relative Capital Flow Model*. Using market action, through a process of reverse engineering, we seek to identify which macro-economic climate is being represented in the market at any given time.

This is an important addition to our discipline as central banks across the globe are attempting to unwind decades of monetary expansion. As this unwinding occurs, it could have significant ramifications for the financial market. Thus, there is an increased need to monitor this process and the corresponding macro-economic result.

In addition to the four scenarios that we have presented in our market notes this year, this month we are including a financial crisis rating.

Inflation – Negative,

Deflation – Negative,

Stagflation – Negative,

Recovery – Neutral,

Financial Crisis – Neutral.

In prior months, our rating for the statistical likelihood of a recovery has been positive, and our rating for the likelihood of a financial crisis has been negative. In the past several weeks, both have changed. The recover scenario has move from positive to neutral and the financial crisis scenario from negative to neutral.

This suggests that the deterioration in the economy and lack of counter-stimulus from the Federal Reserve is negatively impacting the financial markets.

The above scenarios, reflect the current Capital Flow* composite rating of the securities that have historically generated positive returns in the above economic environments.

In addition, our Global Macro Indicators* are as follows for the 7 asset classes we invest in for our clients:

Global Equities – Neutral,

Global Bonds – Negative,

Commodities – Neutral,

Gold – Negative,

U.S. Dollar – Neutral,

Real Estate – Negative

Cryptocurrencies – Negative.

Now, to this month’s report:

As described above, the deterioration in our Recovery and Financial Crisis indicators are merely a reflection of the current performance of the best performing securities when simulated in each scenario. So, we ask, what are the catalysts for the price changes in these securities?

They are the following:

1. Historically high inflation,

2. Rising interest rates,

3. Excessive debt levels,

4. Excessive valuation levels,

5. Recession fears,

6. Geopolitical uncertainties.

Let’s take these one at a time.

Historically High Inflation and Rising Interest Rates

Numbers 1 and 2 go together, as the Fed in an effort to fight inflation, has discontinued their multi-year money printing operation called Quantitative Easing (QE) and is now engaged in Quantitative Tightening (QT).

The theory is that by raising rates, the economy will slow, thereby curtailing inflation. As a result, they are no longer providing the stock and bond markets with excess liquidity which artificially drove stock and bond prices higher and interest rates lower.

No surprise, QT has been bad for stocks bonds and any business that debt financing to stimulate growth.

In the chart below, we can compare inflation today vs. the 1970, which was the last time the US experience high and rising inflation.

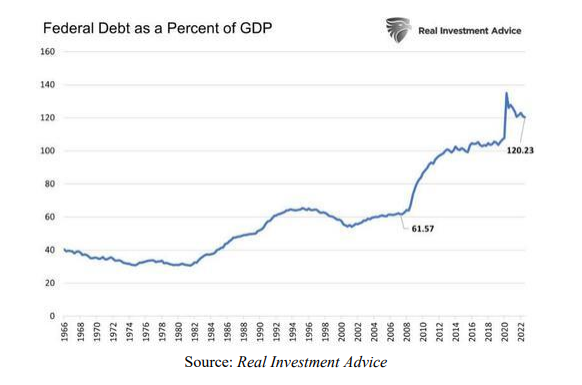

Excessive Debt Levels

As shown below, in the 1970’s, debt levels were dramatically lower. So, can the US economy sustain higher interest rates and inflation today without severe economic consequences?

Since 2008 government debt has risen twice as much as GDP, as shown in the first graph below.

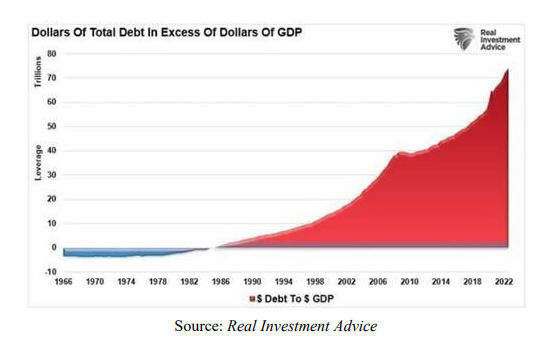

Individual and corporate debt have followed suit.

The next graph below shows over $70 trillion of all debt in the U.S. economy, above and beyond annual GDP. That does not include the present value of future obligations, such as social security, which some budget experts argue can easily double the Treasury’s debt load.

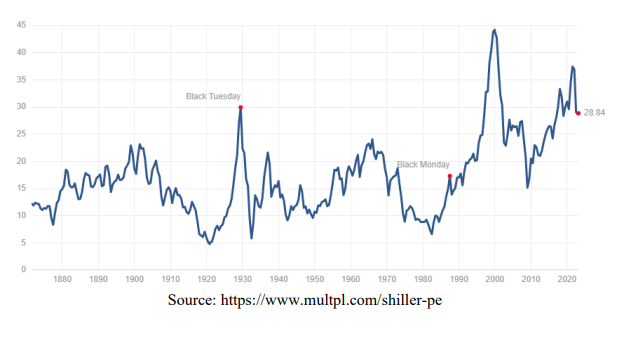

Excessive Valuation Levels

The S&P 500 is still overvalued by historical norms. The Shiller’s cyclically adjusted price-toearnings (CAPE) ratio is currently at 28.84, which according to Robert Shiller is well above its historical mean of 17.

Recession Fears

After several month of declining inflation reports, many analysists are predicting a rebound in inflation in the coming months. If their forecasts are correct, this could force the Fed to choose between raising rate even higher, risking a recession to get inflation down to its 2% target … or waiting to see whether the US can live with much higher inflation.

Neither is a good choice. A recession would certainly be painful, but by waiting, the problem only becomes larger in the future and the impact on the economy and the financial markets becomes even more severe.

Geopolitical Uncertainties

Do stocks go up during war times?

Some of the factors that influence whether stocks go up during war times include the nations involved, the location of the conflict, when the war occurred, the length of the war, and public support for the war.

Any declaration of war has global repercussions, regardless of the size and scope of the conflict. However, the extent to which the financial markets are impacted depends on the details, and historical events don’t necessarily predict market behavior today.

The war in Ukraine appears to be entering a new, more dangerous phase. Historically geopolitical conflicts tend to cause increased market volatility, especially when accompanied by a rising level of uncertainty.

The behavior of the financial markets are heavily dependent on context, as well as myriad internal and external factors that combine to create long-term trends, such as the 5 additional catalysts discussed in this report.

In light of these uncertainties, what should an investor do?

My advice is to pay close attention to our capital flow indicators as summarized at the beginning of this report and described below, and as they change, so should the asset allocation of your portfolio.

In our seven asset classes listed, there are both inflation and deflation sensitive options. It is my belief that it would be prudent for investors to allocate a portion of their assets outside thetraditional markets of stocks and bonds and into alternative asset classes. Some of these are included in our seven assets listed on page 1 of this report.

It is important to note that alternative investments can result in increased portfolio volatility and as with traditional investments like stocks and bonds, are not guaranteed and can decline in value.

Conclusion: Recognizing that we are in uncharted waters with multiple moving parts, we must admit that there is no way to tell in advance exactly how this will unfold. But in such a transitionary environment, the ability to properly anticipate change is predicated upon a detached analysis of information from multiple sources, applying that information to imagine a plausible world different from today’s, understanding how new data points fit (or don’t fit) into that world and adjusting accordingly.

Although this will be no easy feat, our answer at Consilience Asset Management is to employ a discipline that we believe has the ability to circumvent the effects of these uncertainties and disparities between the above noted risks and actual market action. Ultimately, it will be the forces of supply and demand that will drive prices of financial assets higher or lower, regardless of the fundamental, geopolitical, or economic circumstances.

The cornerstone of our process is our Global Macro Capital Flow Model.

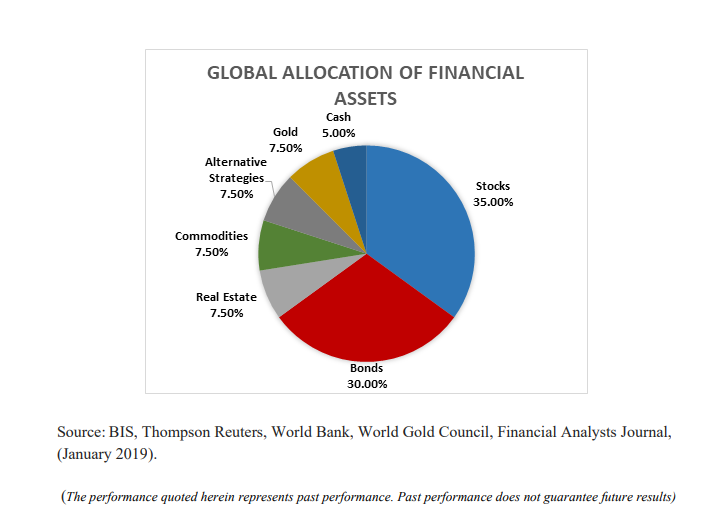

In this model, we monitor the movement of capital among the approximately $250 trillion of tradable global financial assets. Here, market trends can be identified regardless of their driver; debt, geopolitical, economic, or other…

Below is a picture of the distribution of the world’s liquid investment assets as a percent of the $250 trillion total…

By measuring the capital flows of each of these categories relative to the total, both favorable and unfavorable investment trends are identified.

At Consilience Asset Management, we employ this process in deploying client assets.

A more complete description of our model and process can be found on our website: www.consilienceassetmanagement.com under the tab “Our Process.”

Based on this, the ratings for each of the eight asset classes that we monitor are included each month at the beginning of this report.

We are entering a new phase, as the decade-long bull markets for stocks appear to be winding down. We are cognizant of the new challenges inherent due to the structural changes noted in this report, as they will have a huge impact on the current supply/demand dynamics in the global marketplace.

As such, we realize that these are clearly challenging and unprecedented times and therefore it is important for the astute investor to be nimble and pay close attention!

Consilience Asset Management

Roger Faulring – Managing Partner/Portfolio Manager/Market Strategist

Michelle Malone – President/Managing Partner

Donna Stone – Partner/Investment Advisor

Roger Faulring is an Investment Adviser Representative (IAR) with and offers Investment Advisory Services through B. Riley Wealth Advisors, Inc., (BRWA) a SEC Registered Investment Adviser (RIA). BRWA and Consilience Asset Management are not affiliated.

All opinions and estimates included in this communication constitute the author’s judgment as of the date of this report and are subject to change without notice. The information provided is not directed at any investor or category of investors and is provided solely as general information about products and services or to otherwise provide general investment education. None of the information provided should be regarded as a suggestion to engage in or refrain from any investment-related course of action as neither B. Riley Wealth Management nor its affiliates are undertaking to provide you with investment advice or recommendations of any kind. Securities and variable insurance products offered through B. Riley Wealth Management, Inc., Member FINRA/SIPC.

*Our Global Macro Tactical Strategy seeks to identify favorable investment opportunities among seven primary asset classes. Capital is rotated to the specific markets in an effort to control risk by underweighting or eliminating exposure to markets that exhibit elevated risk.

*Our Relative Capital Flow Model is the cornerstone of our tactical allocation decisions and is augmented by our Behavior, Economic, Monetary and Stability indicators.

IMPORTANT NOTICES: The information contained in this electronic message (including any attachments) is privileged and confidential information intended only for the use of the recipient(s). Please notify the sender by email if you are not the intended recipient. If you are not the intended recipient, you are hereby notified that any dissemination, distribution or copying of this communication is strictly prohibited. B. Riley Capital Management, Inc. ("BRCM") does not accept time sensitive, action-oriented messages or transaction orders, including orders to purchase or sell securities, via email or by any other electronic means. BRCM reserves the right to monitor and review the content of all messages sent to or from this email address. Messages sent to or from this email address are stored by a third-party vendor and may be provided to regulators upon request. Neither the sender nor BRCM accepts any liability for any errors or omissions arising as a result of transmission. Any information contained in this electronic message is not an offer or solicitation to buy or sell any security, and while such information has been obtained from sources believed to be reliable, its accuracy is not guaranteed. Any references to the terms of executed transactions should be treated as preliminary only and subject to BRCM's formal written confirmation. This message is for information purposes only and is not an investment recommendation or a solicitation. Past performance is not indicative of future returns. All information is subject to change without notice. Unless indicated, these views are the author's and may differ from those of the firm or others in the firm. BRCM does not represent this is accurate or complete and may not update this information.