If I Were the President, I Would…

Our Market Notes reports are available to you in PDF format. Click below to download.

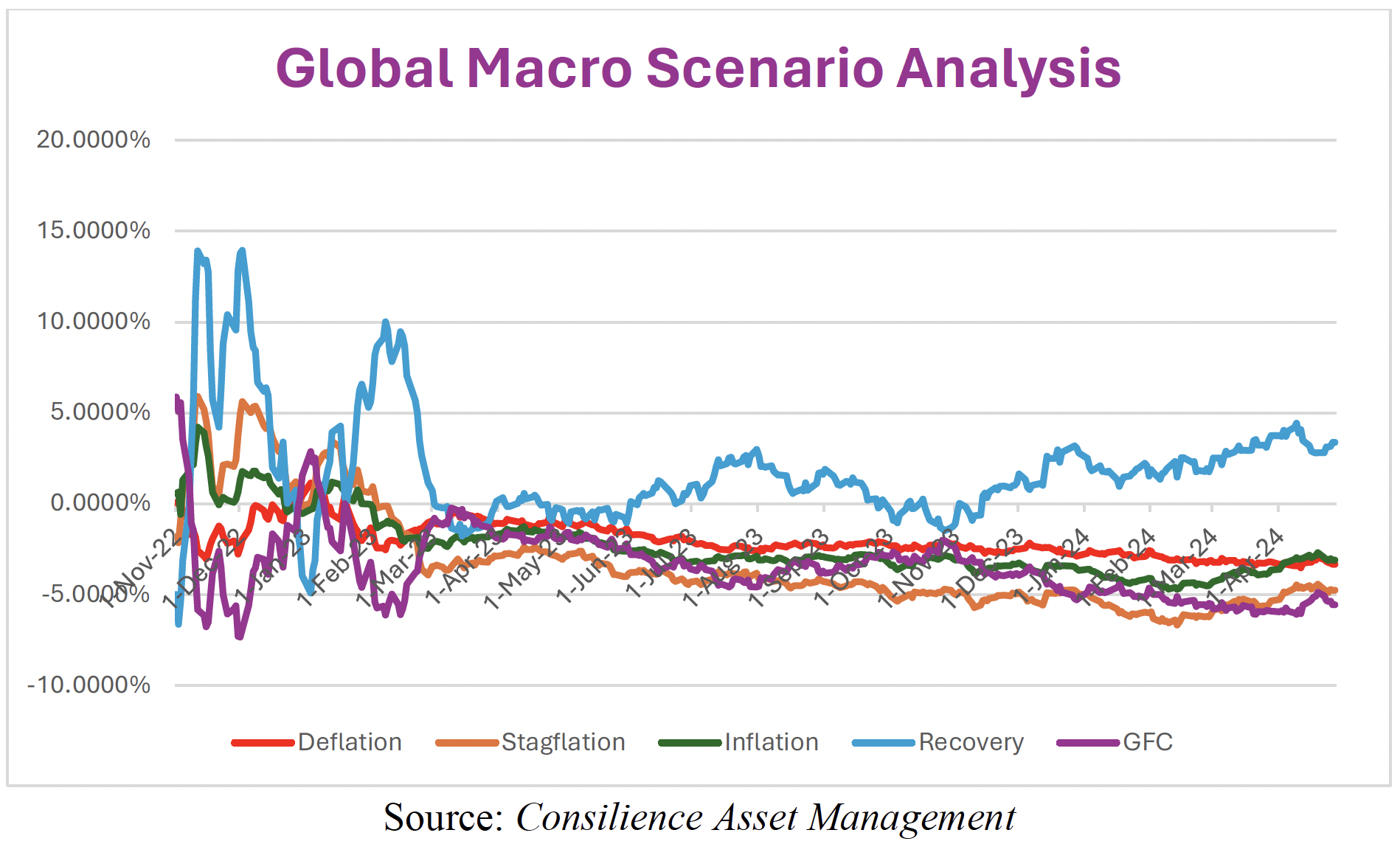

First, an update:

Last year, we at Consilience Asset Management added a Macro-Economic component to our Relative Capital Flow Model*. Using market action, through a process of reverse engineering, we seek to identify which macro-economic climate is being represented in the market at any given time.

This is an important addition to our discipline as central banks across the globe are attempting to unwind decades of monetary expansion. As this unwinding occurs, it could have significant ramifications for the financial market. Thus, there is an increased need to monitor this process and the corresponding macro-economic result.

Below are the ratings of securities in the five scenarios that we are monitoring:

Inflation – Negative,

Deflation – Positive,

Stagflation – Positive,

Recovery – Positive,

Financial Crisis – Neutral.

The above scenarios reflect the current Capital Flow* composite rating of the securities that have historically generated positive returns in the above economic environments.

In addition, our Global Macro Indicators* are as follows for the seven asset classes we invest in for our clients:

Global Equities – Neutral,

Global Bonds – Neutral,

Commodities – Neutral,

Gold – Neutral,

U.S. Dollar – Neutral,

Real Estate – Negative,

Cryptocurrencies – Neutral.

Now, to this month’s report:

If I were the president, I would…

… be very worried.

About inflation, the risk of a recession and declining stock process.

Yet way too many people are convinced that this recent 5% pullback is a blip, nothing more than a hiccup. After all, it’s an election year; there's no way they'll let the market break.

But, last week the Bureau of Economic Analysis (BEA) reported that based on the GDP Deflator (price index), inflation came in at 3.1%, almost double the 1.6% in Q4. Worse, the all-important core Personal Consumption Expenditure (PCE) inflation index for Q1 soared from 2.0% to 3.7%.

So, with inflation still rising, can the Fed begin to cut interest rates, which many believe will be the catalyst for the next upward move in stocks?

Or does the Biden administration have something else up their sleeve that they can pull out in these last few months before the election?

Well… maybe they do have something... courtesy of an unexpected influx of capital gains taxes which hit the treasury on the April 15 IRS deadline. As a result, according to the Congressional Budget Office (CBO), the Treasury's cash level is now well above the ceiling projected.

In fact, according to the treasury.gov site, there is $205 billion more than the Treasury had expected, which if released into the financial system may be a QE like liquidity catalyst for the economy and stocks.

Let’s pause here and reflect on this.

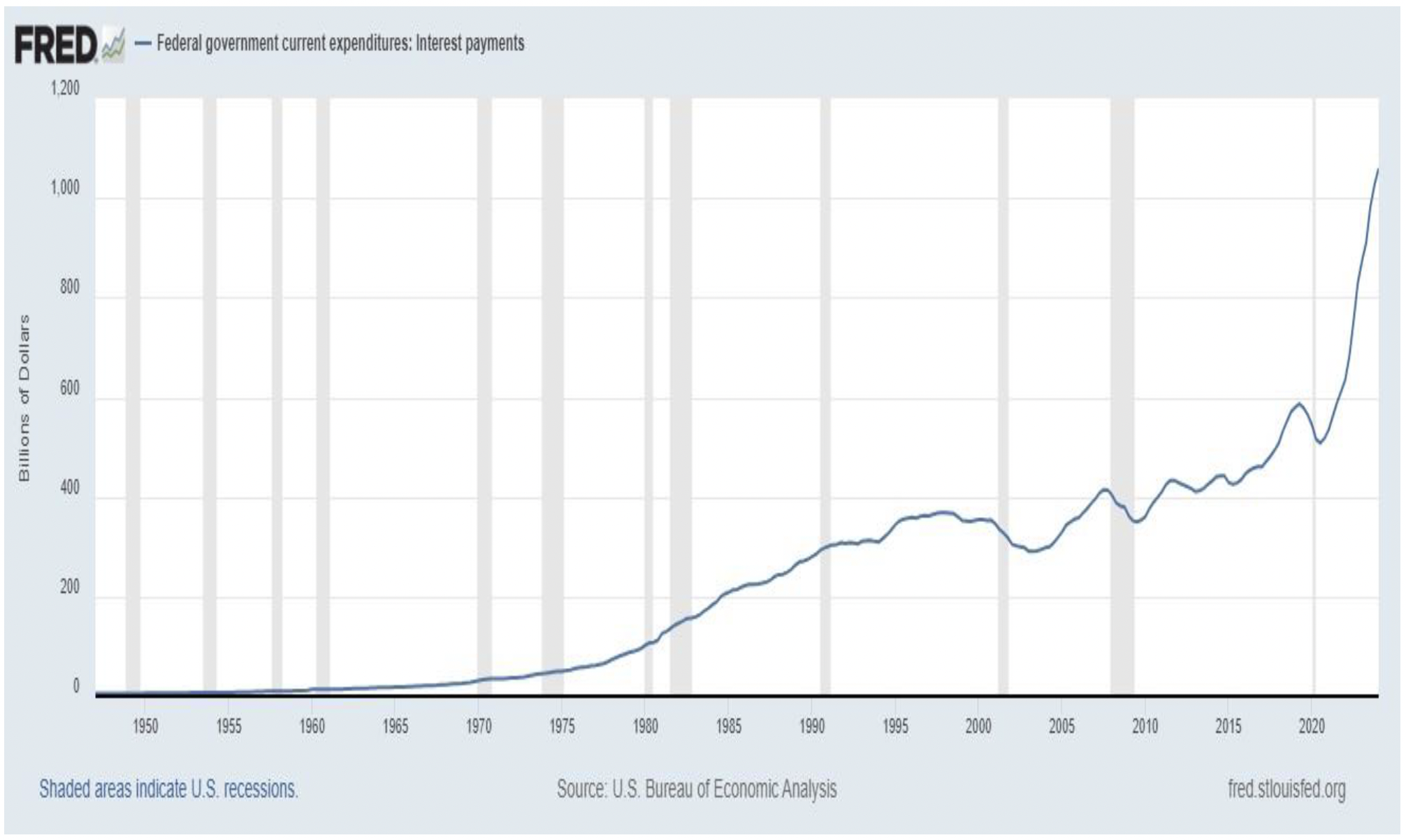

First, let’s consider the broader implications of what the administration and the Treasury may be proposing, that is, releasing $205 of stimulus to give the economy and stock market a final bump in the months leading up to the elections. This at a time when total debt in the US has surpassed $34 trillion,

… the annual budget shortfall exceeds $1 trillion,

and interest costs have topped $1 trillion.

According to David Walker, the former Comptroller General, “That’s irresponsible. It’s unethical, and it’s immoral…”

But will they do it?

Can the markets be fooled that easily? Maybe, as such action could be successful in delivering an artificial short-term fix…

But… in addition to the standard “window-dressing” that occurs in an election year, there may be something more cynical going on.

I have presented the following chart in numerous issues of our Consilience Market Notes which demonstrates the positive correlation between monetary stimulus and rising stock prices.

Taking this one step further, who are the primary beneficiaries of rising stock prices?

No surprise, a disproportionate distribution occurs among the extremely wealthy… those with the greatest stock ownership and greatest political influence.

So… will they do it?

For an answer, we can look to the actions of the world’s Central Banks. Here, something appears to have shifted fundamentally in the last few months. According to Bloomberg, Central Bank gold buying has never been this strong before.

When central banks start to buy gold, that tells you there is evidence of a fundamental shift happening, that there is a further debasement in paper currencies as a result of the massive monetary stimulus/printing campaigns that have been ongoing for decades, especially since the 2008 global financial crisis and which accelerated during the covid outbreak.

Thus, Central Bank’s actions appear to affirm that US monetary expansion will continue, even if it’s through such a method as described above. The acceleration in price inflation that we are now being forced to endure is the direct result of such unprecedented increases in the money supply…

Download here for more information.